At JBI Consulting, we know that understanding industry structure and competitive strategy is vital for business success.

The business landscape is constantly evolving, with new challenges and opportunities emerging every day.

In this post, we’ll explore key concepts like Porter’s Five Forces and generic competitive strategies to help you navigate your industry’s dynamics and gain a competitive edge.

How Industry Forces Shape Competition

The Five Forces Model: A Strategic Framework

Porter’s Five Forces model serves as a powerful tool for businesses to analyze their competitive landscape. This framework examines five key factors that determine the shape of an industry, from internal competition to the negotiating power of customers and suppliers.

New Entrants: Disrupting the Status Quo

The impact of new entrants on an industry depends on entry barriers. In the tech sector, low barriers have led to a surge of app developers, forcing established players to innovate or risk losing market share. Conversely, industries like pharmaceuticals face high barriers (due to regulatory requirements and R&D costs), which limit new competition.

Supplier and Buyer Power: Balancing Act

The power dynamics between businesses, their suppliers, and customers significantly affect profitability. Large automotive manufacturers often hold leverage over smaller parts suppliers, allowing them to negotiate better prices. In contrast, exclusive suppliers in the luxury goods market can command premium prices from brands eager to maintain quality and reputation.

Substitutes: The Silent Threat

Substitutes can erode market share faster than direct competitors. The rise of streaming services (like Netflix and Hulu) decimated the DVD rental market, leading to the bankruptcy of companies like Blockbuster. This example highlights the importance of anticipating and adapting to emerging alternatives that could replace existing products or services.

Rivalry Intensity: The Competitive Battleground

The level of competition within an industry can make or break a business. Mature markets, such as soft drinks (dominated by Coca-Cola and Pepsi), often see fierce competition. This intensity frequently results in price wars and aggressive marketing campaigns, which squeeze profit margins for all players involved.

Understanding these forces is not just theoretical-it’s a practical necessity for survival and growth in today’s business world. Companies that analyze their industry through this lens can identify opportunities to strengthen their position and mitigate threats. While many consulting firms offer industry analysis, JBI Consulting specializes in helping businesses navigate these complex dynamics to achieve sustainable success.

As we move forward, let’s explore how companies can leverage this understanding of industry forces to develop effective competitive advantages.

Crafting Your Competitive Edge

Cost Leadership: Winning the Price War

Cost leadership requires businesses to become the low-cost producer in their industry. Ryanair, Europe’s largest low-cost airline, exemplifies this strategy by focusing on a business model that prioritizes cost reduction. To implement cost leadership:

- Streamline operations: Automate processes and eliminate inefficiencies.

- Optimize supply chain: Negotiate bulk discounts and improve logistics.

- Reduce overhead: Implement lean management practices.

Companies must exercise caution. Cost-cutting should not compromise quality, or they risk losing customers to competitors offering better value.

Differentiation: Standing Out in the Crowd

Differentiation focuses on creating unique products or services that command premium prices. This strategy identifies and communicates the unique qualities of a product or company while highlighting the differences between that product and its competitors. To differentiate effectively:

- Invest in R&D: Develop proprietary technologies or features.

- Build a strong brand: Create emotional connections with customers.

- Offer superior customer service: Exceed expectations at every touchpoint.

Continuous innovation is essential to stay ahead of imitators in a differentiation strategy.

Focus: Dominating Your Niche

The focus strategy involves targeting a specific market segment and becoming the go-to provider for that niche. Tesla initially focused on luxury electric vehicles before expanding to more affordable models. To implement a focus strategy:

- Identify an underserved segment: Look for gaps in the market.

- Tailor your offering: Customize products or services to meet specific needs.

- Build expertise: Become the authority in your chosen niche.

While focus can lead to strong customer loyalty, it also limits market size. Companies should prepare to expand or pivot if market conditions change.

Selecting the Right Strategy

Choosing the right strategy depends on industry dynamics, resources, and capabilities. Companies must analyze their unique situation and develop tailored strategies for success.

Execution and Adaptation

Consistent execution is key to strategy success. Companies should regularly assess their performance and adjust their approach as market conditions evolve. With the right strategy and relentless focus, businesses can carve out a strong competitive position in even the most challenging industries.

As we explore the intricacies of competitive strategy, it’s important to consider how these approaches evolve throughout an industry’s lifecycle. Let’s examine how companies can adapt their strategies to different stages of industry development.

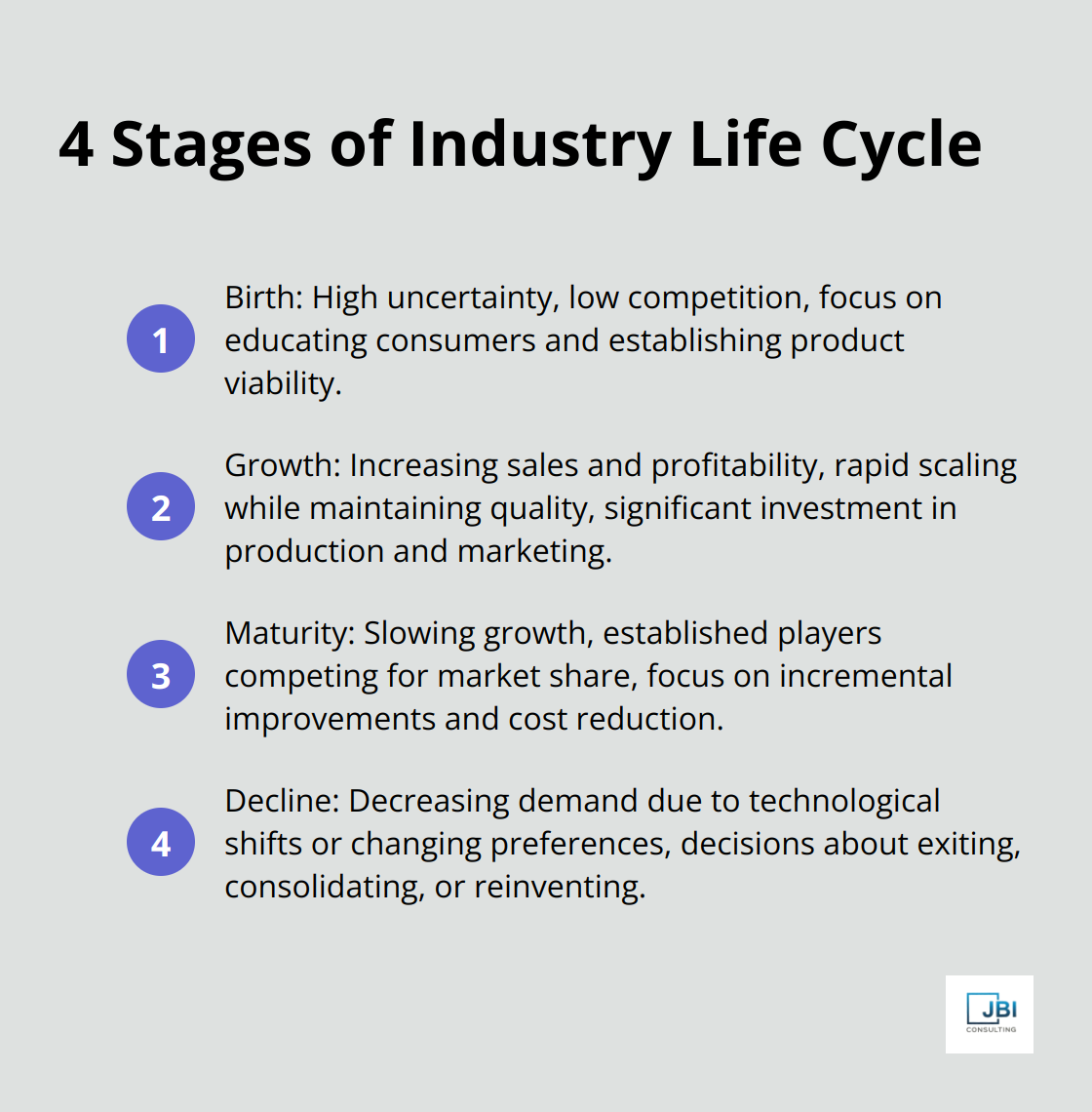

How Industries Evolve

The Birth of an Industry

When an industry first emerges, it presents high uncertainty and low competition. The electric vehicle (EV) market in the early 2000s exemplifies this stage. Tesla entered a nascent industry with few players and undefined market potential. Companies at this stage focus on educating consumers and establishing product viability.

Businesses entering at this stage must remain agile and ready to pivot. Early entrants often shape industry standards but face the highest risks.

Rapid Growth and Increasing Competition

As an industry gains traction, it enters a growth phase marked by increasing sales and profitability. The smartphone industry experienced this in the late 2000s, with Apple’s iPhone and various Android devices flooding the market. During this stage, companies compete to capture market share and establish brand loyalty.

Success in a growing industry requires rapid scaling while maintaining quality. This often necessitates significant investment in production capacity and marketing.

Maturity and Market Share Battles

As growth slows, industries enter maturity. The personal computer market exemplifies this stage, with established players like Dell, HP, and Lenovo competing for market share. In mature industries, innovation often focuses on incremental improvements and cost reduction.

Survival in a mature industry demands efficiency and differentiation. Companies must find ways to cut costs without sacrificing quality.

Navigating Industry Decline

Many industries eventually face decline due to technological shifts or changing consumer preferences. The decline of traditional print media in the face of digital alternatives serves as a prime example. In declining industries, companies must make tough decisions about whether to exit, consolidate, or reinvent themselves.

For those choosing to stay, focusing on a niche market or diversifying into adjacent industries can prove effective.

Adapting Strategies Across the Life Cycle

Aligning business strategies with the industry life cycle is essential. The product life cycle is defined as four distinct stages: product introduction, growth, maturity, and decline. Companies that stay attuned to these changes and adapt their strategies accordingly position themselves for long-term success across the industry life cycle.

Continuous market analysis remains vital throughout all stages. Industries can evolve rapidly (especially in today’s technology-driven world).

Final Thoughts

Understanding industry structure and competitive strategy empowers businesses to thrive in today’s dynamic marketplace. Companies must analyze the forces shaping their industry and adapt their strategies to position themselves for sustainable growth and profitability. The most successful organizations tailor their approach to their unique circumstances and market position, avoiding one-size-fits-all solutions.

Several trends will reshape industry competition in the coming years. Artificial intelligence, sustainability concerns, and the shift towards digital platforms will transform many sectors, creating new opportunities for innovation and disruption. These changes will require businesses to think beyond conventional competitive frameworks and adapt quickly to evolving market conditions.

JBI Consulting helps businesses navigate these complex dynamics and develop winning strategies. Our transformative sales program equips individuals and teams with the tools and mindset needed to excel in today’s competitive landscape. We encourage you to explore how our expertise can help you turn industry challenges into opportunities for growth and success.